This is a classic case of “One size does NOT fit all” as there are vast differences in the justification driving the decisions for different types of vessels. Nevertheless, let’s try to come to some fairly general conclusions on today’s convoluted markets.

During the past 4-6 months, we have seen VLCC asset values skyrocket. In June, one could find an older vessel well before its 4th Special Survey for some US$28 to 30 million. Today, one needs to have well over US$40 million in ready cash to talk seriously about such a ship. Likewise, the cost of a new build has gone from US$90 million 8 months ago to well over US$120 million today. Scrap prices have hovered around US$600 per LDT for such vessels, so the owner who wants to add a VLCC to their fleet needs to have a plan to keep it for a while. The benchmark TD3C charter was yielding owners a Time Charter Equivalent of negative $9,000 per day at mid-year and has improved to a positive US$70,000 per day, today.

LNG Carriers and Pure Car and Truck Carrier prices have moved in the same way and their charter hire rates have gone even higher. We see day rates for large modern LNG vessels of above US$450,000 today. (And there are 2 dozen, at least, parked off EU ports awaiting discharging berths.)

Container ships are heading the other way, with values falling quite alarmingly. However, one of the “Big Boys” is continuing to buy older ships….now having completed the purchase of 250 ships since the start of the pandemic. Yards’ order books are bulging with contracts to build container ships, many of massive size, and one wonders what proportion of these contracts will actually see new vessels entering service.

Will we see an exchange of tonnage in this sector, where relatively young (10 to 12 years) ships are scrapped to make way for new bottoms coming off the production lines? What will that do to scrap prices? This scenario may work well for dedicated liner operators but can spell doom for asset-flipping owners.

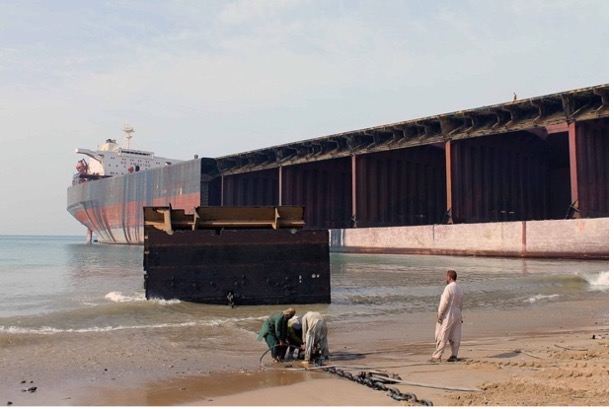

On the subject of scrapping, it seems that there is a dearth of tonnage on offer to scrap yards at the moment. Also, another issue is at play there; a shortage of US dollars in Bangladesh, resulting in banks being unable to offer US-denominated LCs.

Dry bulk vessel prices and charter rates remain reasonably steady…as steady as one may expect in such an unsteady world.

So, an owner who buys ships in order to flip the asset can still do well, although the risks seem to be getting higher daily.

An owner who sees himself as a ship operator rather than an asset trader has a different outlook. We need to go back to our discussion on fuel in order to see what such an owner must consider.

What engine should be installed in a new build? What is the risk of the fuel type selected becoming obsolete, or worse, banned? These issues tend to drive owners away from new builds, and the cautious man may opt for an existing vessel with the idea that by the time she is ready for her trip to Gadani Beach a new technology will have settled the future fuel conundrum.

No doubt at all, our beloved shipping industry is turning faster by the day, and becoming more and more complex, and interesting, as it does so. There is certainly room for the dedicated asset-flipping owner, just as there is room for the long-sighted operating owner. But both need to have the use of crystal balls.